Current portfolio

-

DNS:NET

GermanyCommunications

Digitalisation

Overview

DNS:NET is a leading independent telecommunications provider in Germany. Established in 1998, DNS:NET is rolling out and operating a fibre-to-the home network in outer Berlin, Brandenburg and Saxony Anhalt. 3i Infrastructure’s backing allows DNS:NET to continue its build programme to provide gigabit-ready connectivity to its customers across the region.

Recent Developments

DNS:NET has made significant progress in the ongoing construction of its fibre-to-the-home (‘FTTH’) network; both its owned networks in outer Berlin and Brandenburg and its leased networks in Saxony Anhalt. This is an important achievement given the challenging market conditions for FTTH network rollouts in Germany. It reflects the disciplined and focused approach to network rollout adopted by DNS:NET.

In relation to its ‘owned’ networks, the company has achieved its goal of connecting its existing ‘homes passed’ and ‘homes connected’ infrastructure to the backbone fibre infrastructure. This has led to a significant increase in the number of ‘homes connected and activated’, with customers now receiving a fibre-to-the-home service and DNS:NET earning the associated revenues. DNS:NET is also revisiting its existing networks to connect and activate additional homes (a process referred to as ‘densification’) and is moving into new areas to continue its rollout.

Significant operational improvements have been delivered under the new management team including in relation to sales, marketing, and customer care.

In January 2025, 3iN injected a further £20 million of equity to part fund the next stage of the fibre roll-out.

Investment rationale

In June 2021, 3i Infrastructure plc invested c.€182m to acquire a 60% stake in DNS:NET.

Fibre is superior to other broadband access technologies because it provides reliable low latency, high bandwidth and distance-independent connectivity for both download and upload. Demand for FTTH connectivity is forecast to grow rapidly, as consumers normalise data intensive activities such as cloud-based remote working, high definition streaming and online gaming, and increasingly view high speed broadband as an essential service.

Germany lags behind most European countries in its FTTH deployment, with only 14% coverage today compared to the European average of 33%. The market is projected to grow at 30% p.a. to meet the German government’s objective of every one of its 43 million households having access to gigabit speed broadband by 2025.

Sustainability

DNS:Net is progressing the rollout of its FTTH network in areas around Berlin (Berlin Vicinity) and in the State of Brandenburg. The provision of FTTH is widely recognised as a key driver of regional economic growth and socio-economic benefits and, through the replacement of older copper line technologies, potentially reduces energy consumption. Studies report that the value-added services enabled by high speed internet facilitated by FTTH connectivity can reduce travel requirements, enhance the quality and cost of delivering of local services and improve access to medical advice in rural areas.

Key factsLargest independent fibre-to-the-cabinet (FTTC) network in Berlin>380 employees3 data centres in Berlin

Deal teamAnna Dellis

Deal teamAnna Dellis

Partner

UK / InfrastructureChris Rowland

Director

UK / InfrastructureLorenz Woelfel

Senior Associate

UK / InfrastructureEric Bucher

Associate

UK / Infrastructure -

ESVAGT

DenmarkEnergy

Energy transition

Overview

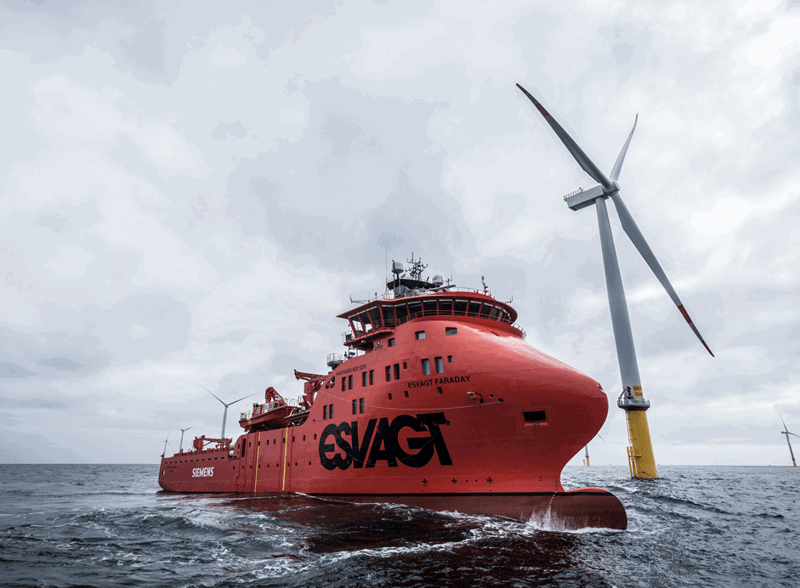

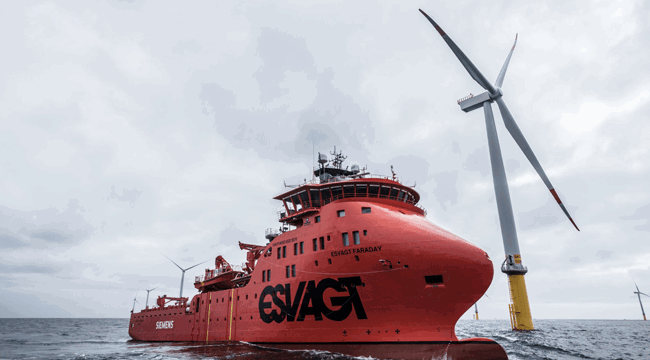

Headquartered in Esbjerg, Denmark, ESVAGT is the market leader in the fast-growing segment of service operation vessels (“SOV”) for the global offshore wind industry. The Company is also a leading provider of emergency rescue and response vessels (“ERRV”) and related services to the offshore energy industry in and around the North Sea and the Barents Sea.

ESVAGT is the pioneer and market leader in the provision of SOVs to offshore wind farms, with nine bespoke vessels in operation and a further four under construction. SOVs are purpose-built, high performance vessels, providing efficient transport of maintenance technicians to wind turbines and other offshore wind equipment, under long term contracts. The offshore wind market, and hence demand for SOVs, is expected to grow strongly over the coming years, creating significant opportunities for the company.

Its ERRV services mainly involve the rescue and recovery of personnel, but also include the dispersion and recovery of oil spills, crew transfers and towing. ESVAGT is the leading provider of ERRV services in Denmark and Norway, with market shares of approximately 100% and 50%, respectively, as well as an established and growing presence in the UK. The majority of ESVAGT’s ERRV revenues are associated with North Sea oil and gas production support, with the remainder generated by supporting exploration activity.

ESVAGT has been operating since 1981, employs over 1,200 people and owns a fleet of more than 40 vessels.

Recent developments

ESVAGT performed in line with expectations during the year.

ESVAGT is the market leader in European offshore wind Service Operation Vessel (‘SOV’) provision, currently operating nine vessels, with an additional four SOVs under construction - three in Europe and one in the US. These vessels are specifically designed to serve long-term charter agreements.

The European offshore wind development pipeline continues to see significant growth, driven by increasing government targets for offshore wind and a heightened focus on energy security. In contrast, the US market is facing uncertainty due to a pause in new offshore wind projects. ESVAGT has also established a joint venture with KMC Line in South Korea, which, if successful, could see ESVAGT becoming the first international SOV operator in the South Korean market, adding an alternative growth market to the business.

ESVAGT’s Emergency Response and Rescue Vessel (‘ERRV’) segment performed strongly, with high day rates and utilisation levels. The ERRV market remains attractive, supported by stable demand and a shrinking supply of available ERRVs to that market, due to vessel attrition and limited new tonnage entering the market.During the year, ESVAGT closed a further €200 million committed debt facility at attractive rates, providing additional capital to support its growth plans.

Investment rationale

3i Infrastructure acquired ESVAGT from AP Møller-Maersk and other minority shareholders in September 2015, in a consortium with AMP Capital.

ESVAGT has strong infrastructure characteristics and operates in an attractive market:

- It is a market leader in Denmark and Norway and has a small but growing presence in the UK offshore oil and gas market and in the expanding North Sea offshore wind sector.

- It is an asset intensive business, with a modern state-of-the-art fleet of purpose-built vessels.

- A high proportion of its revenues is contracted over the medium term with a diverse customer base featuring limited customer concentration, underpinning stable and predictable cash flows.

- It provides an essential service for the offshore energy industry in light of regulatory health and safety requirements, which constitutes a small component of the overall production cost, resulting in lower price sensitivity;

- It operates in a market with high barriers to entry, as customers require bespoke vessels, manned by experienced crews with a strong safety track record. The harsh weather conditions and language barriers also inhibit new market entrants based outside the region; and

- With its leading market position, strong safety track record and state-of-the-art fleet, ESVAGT is optimally positioned to exploit growth opportunities in the UK and potentially further afield, as well as in the offshore wind energy market.

Sustainability

ESVAGT now has over 60% of its contracted EBITDA serving the Wind sector, up from 25% at the time of acquisition. ESVAGT’s US joint venture, CREST, co-owned with Crowley, won its first contract in the US offshore wind market in early 2023 for Siemens Gamesa. In FY24, ESVAGT won two additional SOV contracts with Ørsted and Vestas in the North Sea. ESVAGT also signed a Memorandum of Understanding with KMC Line, a Korean shipping company, to establish a joint venture in South Korea and enter the South Korean wind market.

Key facts>43 vessels in the fleet>1,100 employees14 years average SOV contract length

Deal teamOscar Tylegård

Deal teamOscar Tylegård

Partner

UK / InfrastructureClaudio Ossanna

Senior Associate

UK / InfrastructureAnna Dellis

Partner

UK / InfrastructureAlexi Kirilenko

Director

UK / Infrastructure -

Future Biogas

UKUtilities

Energy transition

Overview

Future Biogas is one of the largest anaerobic digestion (AD) plant developers and biogas producers in the UK. It owns stakes in and operates nine AD plants and operates an additional three AD plants under medium-long term contracts.

Future Biogas’s plants convert a wide range of feedstocks into clean and renewable energy through AD which produces biogas. Biogas can either be used to generate green electricity, or upgraded into biomethane and injected into the UK’s national gas network. Future Biogas produces approximately 700GWh of biogas per year across 12 sites.

Biomethane from AD is a ready-to-use and commercially viable solution for hard to decarbonise industrial sectors. It does not require any upgrade to the existing UK gas infrastructure. Energy produced by AD plants is carbon neutral, as the CO2 released during the process matches the CO2 absorbed from the atmosphere by the feedstock.

Future Biogas promotes a regenerative farming approach, sustainably integrating feedstock from energy crops into agricultural systems. The circular process of returning digestate back to land can help replenish soil nutrients and carbon and displaces demand for carbon intensive artificial fertilisers.

Recent developments

Future Biogas performed ahead of expectations, driven by higher average gas prices and strong production volumes.

In August 2024, the company acquired a 51% stake in a portfolio of six gas-to-grid AD plants from JLEN Environmental Assets Group Limited (‘JLEN’). This investment has increased the operational scale of the company and was an important milestone.

In September 2024, we syndicated a 23% stake in Future Biogas to RWE Energy Transition Investments (‘RWE’) for proceeds of £30 million. RWE brings extensive experience in the broader energy sector, and its investment endorses the potential of the platform and the strategy we are pursuing.

In January 2025, the company completed construction of the Gonerby Moor site, further expanding its operational scale. The site has a 15-year offtake agreement with AstraZeneca for the green gas produced.

In March 2025, we completed a refinancing on favourable terms, increasing the company’s debt capacity to support future growth.

Sustainability

Future Biogas agreed a partnership with AstraZeneca to establish the UK’s first unsubsidised industrial-scale supply of biomethane gas. Energy from the biomethane facility will supply AstraZeneca’s sites in Macclesfield, Cambridge, Luton and Speke with 100 gigawatt hours (GWh) per year, equivalent to the heat demands of over 8,000 homes. Once operational in early 2025, the partnership will reduce emissions by an estimated 20,000 tonnes of CO2 equivalent ‘(tCO2e)’, adding renewable energy capacity to the national gas grid.

Key facts12 AD plants with 1 additional plant under construction+500GWh of biogas produced per yearPromotes sustainable farming practicesLargest producer of biomethane in the UKDeal teamTim Short

Partner

UK / InfrastructureYaad Virdee

Director

UK / InfrastructureNeel Mistry

Associate Director

UK / InfrastructureCharlie Rees

Associate

UK / Infrastructure

-

FLAG

UKCommunications

Digitalisation

Overview

FLAG is a leading global data communications service provider and owner of one of the world’s largest private subsea fibre optic networks. The business provides high-bandwidth connectivity to a range of customers including over-the-top content providers, telecom carriers, new media providers and enterprises.

FLAG’s 66,000km of cables span from North America to Asia. It is particularly strong on the Europe-Asia and Intra-Asia routes where it is well positioned to capitalise on growth opportunities and serve the exponentially growing demand for data traffic.

Recent developments

FLAG has shown strong year-on-year growth in lease revenues and has recently signed several large bulk capacity deals on its Middle East and intra-Asia subsea routes. Financial performance was held back by a high level of cable cuts which have now been repaired. The sales pipeline is healthy and demand for subsea data

capacity continues to grow, driven by increasing adoption of AI applications and substantial investments in capacity and route diversification by the hyperscalers.

Looking ahead, FLAG is evaluating several attractive growth opportunities, for example, acquiring new subsea capacity and developing new edge data centres near its cable landing stations that will drive additional data on its subsea network.

Investment rationale

In November 2021, 3i Infrastructure plc agreed to invest c.$512m to acquire a 100% stake in GCX (subsequently renamed FLAG). Additional acquisition debt was raised in March 2022, reducing the Company's equity commitment to $377m. The investment completed in September 2022.

- FLAG owns one of the most comprehensive subsea cable networks globally, serving customers in over 180+ countries

- Benefits from the rapidly expanding data market with data usage forecast to grow exponentially

- Operates in a market with high barriers to entry whilst providing an essential service

- Supported by a highly experienced management team who have a strong track record in the sector

Sustainability

As a leading global data communications service provider and owner of one of the world’s largest private subsea fibre optic networks, FLAG enables increased connectivity to underserved regions in Asia, Africa and Middle East. The business is continuously developing solutions to maximize the efficiency, utilisation and capacity of existing assets and systems, reducing environmental impacts. FLAG is actively developing an ESG strategy to enhance its environmental, social and corporate governance. In addition, the business is in the process of certifying its carbon footprint and working on emission reduction initiatives.

Key facts>180 countries Customers in over 180 countries>35 countries Access to landing stations in over 35 countries50,000km Cables spanning 50,000km from North America to AsiaDeal teamTim Short

Partner

UKPaolo Bergamelli

Director

UK / Infrastructure

-

Infinis

UKUtilities

Energy transition

Overview

Infinis had a strong year, generating a value gain of £61 million, driven by higher than forecast levels of exported power from its captured landfill methane business.

Strategically, Infinis is ideally placed to scale its electricity generation capabilities by developing solar and battery projects on brownfield and landfill sites, which offer attractive fundamentals including expedited grid connectivity. The company is making material progress on its 1.4GW pipeline of solar and battery storage assets. During the year, Infinis commenced construction on 150MW of solar capacity and secured planning consent for an additional 134MW.

Despite ongoing industry-wide planning challenges, the company obtained approvals for a further seven solar projects in the second half of the year. Infinis maintains a confident outlook for its solar platform, supported by a strong pipeline and favourable market tailwinds.

- Captured methane: 255 MW across 104 sites

- Solar: 103 MW across 4 sites

- Flexible generation: 173 MW across 29 sites

This unique combination of green baseload power, renewable assets and flexible generation mean Infinis is ideally placed to respond to growing electricity demand, increasing energy market volatility and to play a key role in the UK’s route to decarbonisation and greenhouse gas reduction.

Recent developments

Infinis had a strong year, generating a value gain of £61 million, driven by higher than forecast levels of exported power from its captured landfill methane business.

Strategically, Infinis is ideally placed to scale its electricity generation capabilities by developing solar and battery projects on brownfield and landfill sites, which offer attractive fundamentals including expedited grid connectivity. The company is making material progress on its 1.4GW pipeline of solar and battery storage assets. During the year, Infinis commenced construction on 150MW of solar capacity and secured planning consent for an additional 134MW.

Despite ongoing industry-wide planning challenges, the company obtained approvals for a further seven solar projects in the second half of the year. Infinis maintains a confident outlook for its solar platform, supported by a strong pipeline and favourable market tailwinds.

Investment rationale

The investment in Infinis is foremost a yield play. Its front-ended cashflows balance other recent investments by the Company in more growth-oriented businesses. Revenues are underpinned by the inflation-linked UK Renewables Obligation Certificate (“ROC”) regime until 2027. Infinis could also become a platform to make new investments in activities such as distributed power generation from other gas sources, distributed energy storage by exploiting the business’s spare engine and grid connection capacity, and additional landfill gas sites.

Infinis and its market

Infinis is the largest generator of electricity from LFG in the UK, with a portfolio of 121 landfill sites and total installed capacity of over 300MW. LFG is produced by decomposing organic matter in landfill sites. If released into the atmosphere unchecked, LFG contributes to pollution and is a potent greenhouse gas. By extracting LFG from landfill sites, Infinis fulfils an essential role in helping landfill operators meet their environmental compliance obligations. By using the collected LFG to generate electricity, Infinis supplies distribution networks with a consistent source of baseload power.

Sustainability

Infinis’ activities support the UK’s journey to net zero in several key ways:

- Methane is a greenhouse gas. Methane emissions cause 25% of global warming today, with a major surge over the past 15 years. By capturing methane from landfill sites and disused coal mines, Infinis fulfils an essential role in helping landfill operators meet their environmental compliance obligations and contributing to the UK’s reduction of greenhouse gas emissions. By using the captured methane to generate electricity, Infinis supplies distribution networks with a consistent source of green baseload power.

- The government views solar power as key to achieving UK energy independence, with plans to deliver up to 70GW by 2035. Infinis’ ability to deliver solar, including on challenging brownfield and landfill sites, increases the contribution of renewables to the UK’s generation mix. Its continued investment in renewable energy is helping the UK reduce its reliance on fossil fuels.

- Flexible generation provides support for the grid as intermittent renewable generation increases, enabling a stable supply of electricity to UK homes and businesses to be maintained.

Infinis' broader sustainability strategy revolves around creating value for its stakeholders, through protecting health, wellbeing and safety, reducing carbon emissions, eliminating exploitative work and improving diversity and inclusion.

Key facts>130 operational sites531 MW of installed capacity217,000 tonnes of captured methane in FY24

-

Ionisos

FranceSocial infrastructure

Demographic change

Overview

Ionisos is a leading owner and operator of cold sterilisation facilities servicing the medical and pharmaceutical industries. Established in 1993 in France, Ionisos is one of the largest cold sterilisation providers globally and operates a network of 11 facilities in Europe with market leading positions in France and Spain. It has over 250 employees and a highly diversified customer base of around 1,000 customers.

Ionisos delivers a mission-critical, non-discretionary service for customers, for whom cold sterilisation is an essential component of the manufacturing process. It is typically applied to single use products that would be damaged by the heat and/or humidity of hot sterilisation methods.

Recent developments

Ionisos continues to experience growing demand across its core medical and pharmaceutical segments. To maintain this momentum, the company continues to advance its growth initiatives, including a capacity extension of its Kleve Ethylene Oxide (‘EO’) facility in Germany and development of a new X-ray plant in France. As part of its network optimisation, Ionisos is also preparing to decommission two smaller EO sites.

At the same time, the business has strengthened its corporate functions to support future growth. These initiatives, together with softer demand in the non-core industrial cross-linking segment and the forthcoming site closures, have weighed on returns for the period.

Investment rationale

3i Infrastructure acquired Ionisos in September 2019, having committed to invest in July 2019.

- Diversification of 3i Infrastructure’s sector exposure and increased presence in the French market

- Sound market fundamentals with non-cyclical drivers, including an ageing population in Western Europe

- Growing demand for healthcare services increasingly relying on single use medical equipment

- Increasingly stringent regulation governing the sterilisation of medical, pharmaceutical and cosmetics products

- High barriers to entry

- Platform potential with growth opportunities organically and through M&A

Sustainability

Ionisos supports public health by providing sterilisation of medical devices, ensuring that single use products are safe for medical use. Ionisos was one of the first two companies in the 3i Infrastructure portfolio to set an SBT (science-based emissions reduction target) through the Science Based Targets initiative (SBTi). This was achieved via the SME pathway which requires a 42% reduction in Scope 1 and 2 emissions to 2030 from a 2021 baseline, and a requirement to measure and reduce Scope 3 emissions. Ionisos plans to achieve this by improving electricity sourcing (e.g. from renewables), and reducing natural gas consumption on EO sites.

Key facts> 250 employees11 facilities across four countries in Europe>1000 customers

Deal teamPhil White

Deal teamPhil White

Vice Chair of Infrastructure

UK / InfrastructureAaron Church

Partner

UKMarta Pinto

Senior Associate

UK / Infrastructure -

Joulz

BeneluxEnergy

Energy transition

Overview

Joulz is a leading owner and provider of essential energy infrastructure equipment and services in the Netherlands. Joulz serves approximately 21,000 industrial, commercial, and public sector clients with its solutions, that encompass realization, maintenance, management, and leasing of energy infrastructure equipment.

Joulz’ service offering includes mid-voltage infrastructure (owning and leasing transformers, switchgear and cables under long-term contracts), storage (owning and leasing large scale battery storage systems under mid- to long-term contracts), solar (large-scale installations under operational lease or with government-subsidized PPAs), metering (owning and leasing 50,000 electricity and gas meters under mid-term contracts) and EV charging (AC and DC charge points in mid-term exploitation, rental or CPO contracts). Additionally, it provides integrated solutions to address energy transition challenges such as grid congestion.

Recent developments

Joulz delivered a good performance during the year, supported by the commissioning of new electrical infrastructure projects for customers.

The company operates in the Netherlands, where the shift towards a low-carbon economy is driving strong demand for electrification and sustainable energy solutions. Joulz provides tailored infrastructure to support businesses and industrial users in meeting their decarbonisation objectives under medium-to-long term energy-as-a-service contracts. Its integrated energy solutions enable customers to operate and expand their businesses with reliable, scalable and lower-emission energy.

The business is currently advancing several large projects for both individual customers and whole business parks, which will help drive future growth.

Investment Rationale

3i Infrastructure acquired Joulz in April 2019, having committed to invest in March 2019.

- Strong established asset base as well as good potential for growth

- Joulz is set to benefit from the Dutch government’s commitment to decarbonise the economy (the ‘Energy Transition’)

- The Energy Transition is expected to increase electricity consumption and demand for Joulz’s equipment and services

- 3i Infrastructure has relevant experience from investing in the Netherlands and previous investments in the electricity and leasing sectors

Sustainability

In 2023 Joulz installed solar capacity of 14MWp taking cumulative owned capacity to 36MWp by the end of the year. The business is also investing in battery storage systems and EV charging infrastructure. These offerings combined with traditional energy infrastructure (such as transformers and meters) have enabled Joulz to become a leader in providing integrated solutions to businesses in the Netherlands.

Key factsc.260 employeesc.21,000 customersOperates c.53,000 metering assets, c.18,000 medium-voltage assets and c.6,000 EV assets Deal teamAaron Church

Deal teamAaron Church

Partner

UKPhil White

Vice Chair of Infrastructure

UK / InfrastructurePaolo Bergamelli

Director

UK / InfrastructureNeel Mistry

Associate Director

UK / InfrastructureCharlie Rees

Associate

UK / Infrastructure -

Oystercatcher

SingaporeTransport & logistics

Renewing essential infrastructure

Overview

Oystercatcher is the holding company through which the Company holds a 45% interest in Advario Singapore Limited (previously Oiltanking Singapore Limited).

Advario Singapore is a 1.3 million cubic metre facility focused on storage and blending of refined clear petroleum products for a range of blue chip customers. With a premier location, on Jurong Island, it is accessed by pipeline, sea going vessel and barge.

Oiltanking is one of the world’s leading independent storage partners for oils, chemicals and gases, operating 41 terminals in 18 countries with a total storage capacity of 16 million cubic metres.

Recent developments

Oystercatcher’s 45% owned terminal Advario Singapore delivered a strong performance for the year. Although the oil products market remained in backwardation, demand for storage in Singapore and the broader region remained strong and provided a favourable backdrop for Advario Singapore’s commercial discussions, which resulted in rate increases as contracts were renewed. Advario Singapore has also seen an increase in customer activity, leading to high blending and throughput volumes. Advario Singapore continues to be the leading gasoline storage and blending facility in Singapore, as well as in the wider region.

The company, which secured its first sustainable aviation fuel (‘SAF’) storage and blending customer in 2023, is working with its customers to identify opportunities to support them in their ambitions around renewable fuels.

In February 2025, Oystercatcher raised Singapore Dollar denominated holdco debt. This funded a £96 million distribution from Oystercatcher to 3iN. This was in addition to a further £12 million distribution from cash generated by the company.

Sustainability

Advario Singapore has recently converted storage facilities to enable sustainable aviation fuel (‘SAF’) storage, and supported its first SAF storage customer. This has provided the business with a first mover advantage in the SAF storage market in the region, and Advario Singapore is well placed to capture additional SAF storage demand in the future, as the market evolves.

Key facts1.3 million cubic metre facility45% ownership

Deal teamAaron Church

Deal teamAaron Church

Partner

UK / InfrastructureAnna Dellis

Partner

UKOliver Müllem

Director

Germany / InfrastructureMarkus Abeler

Associate

UK / Infrastructure -

SRL Traffic Systems

UKTransport & logistics

Renewing essential infrastructure

Overview

SRL, is the market leading temporary traffic management equipment (“TTE”) rental company in the UK. SRL offers its customers a full-service rental solution, which includes the planning and design of traffic management systems, installation, maintenance and integration with existing systems, as well as direct sales of equipment manufactured by SRL.

SRL’s market-leading reputation is supported by its national depot network, providing a 24/7, 365 days a year service on which customers rely for quick deployment and reactive maintenance work.

Recent developments

SRL specialises in providing equipment to support complex roadworks that require a service component in addition to pure asset rental. The company operates the largest depot network of intelligent traffic management systems in the country, providing installation, monitoring, servicing, maintenance and battery exchange services.

SRL performed significantly behind expectations during the year, caused by a slowdown in activity from local authorities and the telecoms sector, combined with competitive pressure impacting rental rates. Short-term market conditions remain challenging, and we have taken action to cut costs to respond to this. The reduction in value of this investment reflects the under performance in the period and a more prudent view on its outlook.

Investment rationale

3i Infrastructure acquired SRL in December 2021.

- TTE is mission-critical to the safe use of roads

- SRL fits with the Company’s strategy of investing in companies with leading market positions and barriers to entry, yet with operational levers to achieve attractive returns for shareholders through active asset management

- SRL has sound market fundamentals through the increasing emphasis placed on health and safety, and a growing propensity to rent rather than own TTE

- Outsourcing ownership of TTE makes economic sense for traffic management companies, as it allows them to more efficiently manage maintenance and utilisation

- SRL has a market leading reputation and is trusted by its customers

Sustainability

SRL's temporary traffic solutions enable greater segregation and control of traffic flows, in turn improving safety and reducing congestion around roadworks. This improves satisfaction for road users and local communities and reduces pollution. In addition, focus is being placed on health and safety through the use of more sophisticated methods of traffic management to protect highway workers and segregate traffic, cyclists and pedestrians

Key facts24/7 service with access to any location within two hours30 strategically located depots in the UKc.13,000 pieces of equipment under full service contracts

Deal teamJames Dawes

Deal teamJames Dawes

Chief Financial Officer

UK / InfrastructureYaad Virdee

Director

UK / InfrastructureClaudio Ossanna

Senior Associate

UK / InfrastructureLaura Kaps

Associate Director

UK / InfrastructureEric Bucher

Associate

UK / Infrastructure -

Tampnet

NorwayCommunications

Digitalisation

Overview

Tampnet is the leading independent offshore communications network operator in the North Sea and the Gulf of Mexico. It is headquartered in Norway, with operations in the UK, Scandinavia, Netherlands and the USA.

Tampnet provides high speed, low latency and resilient data connectivity enabling the digitalisation of offshore industries. Its unique network includes over 5,400km of fibre optic cables, 200 microwave links, 600,000 km2 of 4G/5G coverage and connects to 40 data centres in 12 European and American cities and central hubs. It operates across four main business areas: fixed installations, mobile rigs and vessels, roaming for offshore workers and international onshore carriers. The majority of its business involves providing fixed fibre links to the offshore energy industry with significant growth coming from emerging digital use-cases and new offshore markets.

Recent developments

Tampnet outperformed expectations in the year, generating a value gain of £32 million. It exceeded both revenue and EBITDA targets, driven by increased offshore activity, particularly in the Gulf of Mexico, and ongoing demand for bandwidth upgrades.

Tampnet is experiencing growing demand for connectivity as AI and digitalisation drive increased bandwidth requirements, alongside a heightened focus on crew welfare solutions. The company has partnered with Armada to deliver edge data centres and advanced AI-driven applications to its offshore customers.

Tampnet’s private networks business continues to grow, with 19 private networks already installed. The company is encouraged by the strong momentum in this segment and is actively working with several customers to design technical connectivity solutions for carbon sequestration projects within its existing network in the North Sea.

Investment Rationale

3i Infrastructure acquired 50% of Tampnet in March 2019 alongside Danish pension fund ATP, having committed to invest in July 2018.

- Tampnet’s fibre optic links provide customers with mission-critical reliable communications

- Benefits from the growing requirement for high bandwidth and low latency in data networks

- More than 50 customers including oil and gas operators, offshore service providers and telecom operators

- Opportunity to grow into new segments such as offshore wind, commercial vessels and the point-to-point carrier segment

Sustainability

Tampnet is leveraging its infrastructure and expertise in connectivity and digitalisation to support an array of growing sectors offshore. This year Tampnet has entered the carbon sequestration market by supporting a number of North Sea projects in their design phase, enabling them to connect to Tampnet's network as soon as they go live. Additionally, Tampnet acquired dasNetz, a leading provider of offshore wind connectivity in the German part of the North Sea, as part of a strategy to continue expanding in offshore wind and renewables.

Key facts1,200km offshore cable system acquired in 2020>50 customers in multiple sectorsWorld’s largest offshore high-capacity communication network

Deal teamOscar Tylegård

Deal teamOscar Tylegård

Partner

UKBernardo Sottomayor

Managing Partner, Co-Head of European Infrastructure

UK / Executive CommitteeChris Rowland

Director

UK / InfrastructureLorenz Woelfel

Senior Associate

UK / InfrastructureMarkus Abeler

Associate

UK / InfrastructureAlexi Kirilenko

Director

UK / Infrastructure -

TCR

BeneluxTransport & logistics

Renewing essential infrastructure

Overview

Headquartered in Brussels, Belgium, TCR is the largest independent lessor of airport ground support equipment (“GSE”). It operates at more than 230 airports across more than 20 countries. Since inception, TCR has defined the market for leased GSE, providing high quality assets and a full service leasing, maintenance and fleet management offering to its clients, which are predominantly independent ground handling companies, airlines and airports. This enables GSE operators to concentrate on their core business of ground handling.

TCR’s GSE is the essential mobile infrastructure used to service aircraft on the ground and enable airports to handle passengers, luggage and cargo, with upwards of 30 pieces of equipment required per turnaround. Reliable GSE is critical to the smooth operation of airports and timely movement of aircraft, and TCR is able to deliver this with its access to scarce airside repair workshops, which provides a high barrier to entry. Sustainability is at the heart of the business and its mission is to deliver the most efficient and sustainable GSE services. Through its expertise in GSE fleet optimisation, “pooling” initiatives and the provision of green GSE, TCR is playing a key role in enabling the decarbonisation of airport ground operations in the airports where it operates.

Recent developments

TCR performed well in the year, driven by higher fleet utilisation rates and accelerated expansion into new markets. The broader macro environment has been supportive, with aviation activity now exceeding pre-pandemic levels. Higher interest rates are favourable to ground support equipment (‘GSE’) lessors, while growing decarbonisation efforts, particularly in Europe, have increased demand for electric-powered GSE and also equipment pooling arrangements to improve efficiency.

During the year, TCR secured several key contracts, including an exclusive contract to supply a centralised all-electric GSE pool at JFK International Airport New Terminal One. This marks a significant step forward in TCR’s North American presence and provides a strong platform for further growth in this largely untapped market for the company.

In February 2025, we completed a debt refinancing on attractive terms, supporting future growth and enabling a substantial distribution of £60 million to 3iN.

Investment rationale

TCR fits with the Company’s strategy of investing in companies with good asset backing, strong market positions and barriers to entry, yet with operational levers to achieve attractive returns for shareholders through active asset management:

- GSE is a scarce resource that is critical to the functioning of an airport; through first mover advantage, TCR has benefited from securing the largest independent GSE fleet in Europe. TCR has access to maintenance workshops in prime locations at airports, many of which are located airside. This means that a high quality maintenance and asset management service can be provided, resulting in high availability of TCR’s fleet.

- TCR is able to offer full-service rentals on a pan-European basis. This creates competitive advantages against competitors, which tend to offer either dry leases or only repair and maintenance services. TCR’s network means it can offer pan-European solutions at multiple locations, matching the footprints of its customers.

- Outsourcing ownership of GSE equipment makes economic sense for independent ground handlers, as it allows them to manage the mismatch between short-term handling contracts and the typically 10-15 year useful life of equipment.

- TCR’s rental contracts are aligned with the ground handlers’ contracts with the airlines and are typically 3-5 years in duration. TCR has experienced a high level of contract renewal.

- The business has a diversified portfolio and is present at over 180 airports across 18 countries with a diverse contract and customer base meaning the revenues of the business are not materially reliant on a single client or geography.

- The investment will provide exposure to the long-term growth in the aviation market, which is fundamentally GDP driven, yet it is expected to be insulated from short-term shocks to demand due to its exposure to aircraft movements rather than passenger numbers.

Sustainability

TCR’s significant growth is supported, amongst other drivers, by the ambition of most European airports to decarbonise their operations on the apron. TCR is helping its customers implement electric replacement plans where airport charging infrastructure allows, and working on a diesel-to-electric GSE conversion strategy where replacement is not feasible. In 2023, the business has grown its electric fleet by 22%. The business is also working on the development of innovative end-to-end sustainability solutions to support its customers’ decarbonisation journey, such as ‘chargingas-a service’ solutions.

Key facts>210 airports Operates at over 210 airports>1,600 employeesc.36,000 ground support equipment assets